Biopharma M&A and Strategic Collaboration Insights (Q3'23)

The latest edition of Oppenheimer & Co. Inc.’s Quarterly Biopharma M&A and Strategic Collaboration Insights Report is now available upon request.

Key Takeaways:

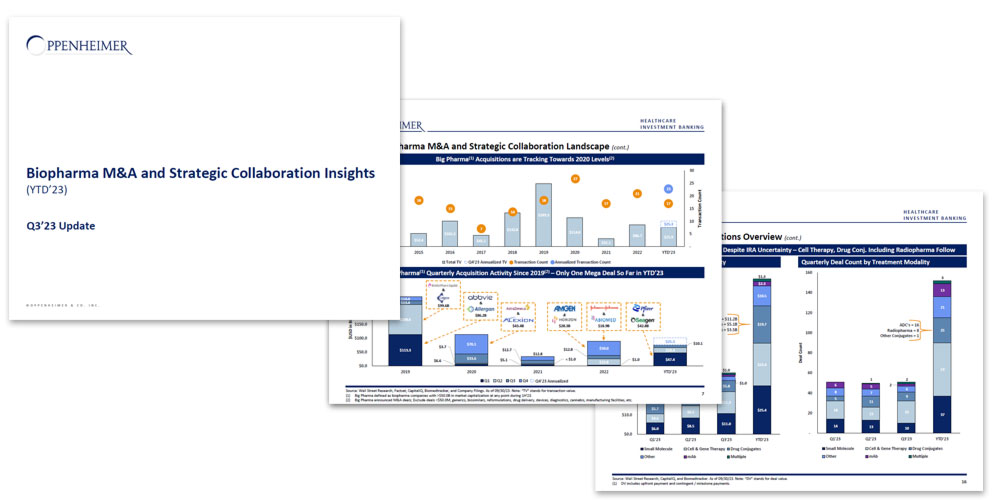

YTD’23 M&A Activity Has Already Cleared FY’21 – Normalizing for Mega Deals, FY’23 Tracking to Surpass FY’20

- 2023 Biopharma M&A started off very strong with the $42.8B acquisition of Seagen and several notable $1B+ acquisitions including Prometheus Biosciences, IVERIC bio, Chinook Therapeutics, Provention Bio, Inversago, and Reata Pharmaceuticals

- Additionally, there has been considerable acquisitions of assets in YTD’23, including Bausch + Lomb’s purchase of Novartis’ XIRDA for $2.5B, Amphastar Pharmaceuticals’ acquisition of Baqsimi for $1.1B, and Alexion’s acquisition of Pfizer’s gene therapy (AAV) programs for $1.0B (all amounts include milestones)

- At a high level, Q3’23 activity contracted from a very strong Q2’23 in terms of total TV and volume – Nonetheless, a very positive and notable quarter for M&A:

- If the Pfizer / Seagen deal is excluded from Q1’23, Q3’23 had 22% more total TV and only one less deal than Q1’23 at 13

- Share price premiums for publicly traded targets in Q3’23 shrunk significantly: ~82% vs. ~122% in Q2’23 – EV multiples remained relatively flat around 2.0x

- Commercial and clinical stage companies make up the vast majority of YTD’23 M&A activity (~64% and ~31% of total TV) – Biologics (ADCs and mAbs) continue to be a favorite among acquirers, while there is still significant interest in small molecule M&A despite the IRA legislation

- Q3’23 Strategic collaboration activity was virtually identical to Q1’23 and Q2’23 in terms of volume; however, total deal value continued to rise, particularity in the form of milestone payments despite the continuing challenges in the equity market

- Collaboration deals for CV & Metabolic companies spiked during Q3’23 largely due to the Roche / Alnylam ($3.1B) and Novo Nordisk / Valo Health ($2.8B)

- Small molecules, ADCs, and especially cell & gene therapy focused companies remain the hottest targets for partnerships on a treatment modality basis

- Interest in Discovery / Platform companies continued in Q3’23, particularly in AI Discovery ($5.5B in Q3’23 alone)

Deal Catalysts

- Excess cash reserves at Big Pharma and large biotech and the need for top line growth

- Steep and fast-approaching patent cliff for Big Pharma

- Mega-blockbusters set to lose exclusivity over the next six years represent the biggest threat to commercial drug sales in decades

- Three drugs facing near-term loss of exclusivity have generated $50.2B in combined LTM global revenues alone: Merck’s Keytruda ($22.9B), AbbVie’s Humira ($18.7B), and Bristol Meyer’s Opdivo ($8.6B)

- A challenging IPO market underpinned by low biotech valuations

- Profound clinical data and positive newsflow

- Declining COVID-19 vaccine revenue

Deal Headwinds

- Ambiguous macroeconomic outlook coupled with rising costs / inflation concerns

- Increased FTC scrutiny (e.g. FTC issued Opinion and Order for Amgen / Horizon and Illumina / Grail)

- Fragile supply chains and escalating costs of talent / human capital

- Decreasing risk appetite to take on early-stage programs whose funding requirements will eat into profits

- Bottom line P&L impacts from the new drug price negotiation legislation beginning in 2026 signed in to law through the IRA

Please reach out to Michael Margolis, R.Ph. (MichaelA.Margolis@opco.com), Daniel Parisotto, Ph.D (Daniel.Parisotto@opco.com), or Robert Lewis (Robert.Lewis@opco.com) directly to request a copy.

This notice is provided for informational purposes only, and is not intended as a recommendation or an offer or solicitation for the purchase or sale of any security or financial instrument. Nothing contained herein shall constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation would be prohibited.

This notice may contain statistical data cited from third-party sources believed to be reliable, but Oppenheimer & Co. Inc. does not represent that any such third-party statistical information is accurate or complete, and it should not be relied upon as such. All market prices, data and other information are not warranted as to completeness or accuracy and are subject to change without notice.

2023 Oppenheimer & Co. Inc. Transacts Business on all Principal Exchanges and Member SIPC 6017925.1