Navigating the Flux: Insights for a Dynamic Market

Equity markets began February strongly but have since pulled back to support levels, driven by uncertainty over tariffs, extensive government reforms, and geopolitical tensions—all visibly impacting prices. With tariffs nearing and trade policies shifting, the US dollar and yields have weakened, suggesting expectations of Federal Reserve rate cuts; oil prices have fallen, could be pointing to recession risks, while gold’s decline aligns with hopes of a soft landing.

This inconsistent price movement reflects deep market indecision. We’ve consistently noted that uncertainty fuels volatility, now driving investor sentiment to extremes—CNN’s Fear and Greed Index registers “extreme fear.” A market peak may be near, yet it lacks the risk-on exuberance typically seen at tops. The S&P 500’s technical strength holds, raising a key question: further declines or an opportunity?

Commentary leans heavily bearish on these issues, but few highlight potential benefits from such significant changes. Could short-term disruption lead to long-term economic gain? History suggests markets often rise despite unfavorable conditions, climbing the “wall of worry.” As February ends, attractive risk/ reward scenarios emerge. We await signs of stabilization that might indicate an uptrend’s return.

Fixed Income

As markets adjust to the administration’s extensive changes, we’re seeking opportunities in the bond market. We’re directing clients toward call-protected positions, ensuring consistent yields as money market and short-term rates decline. The Fed’s gradual approach to rate cuts offers a chance to secure higher yields—key amid emerging economic pressures. With government job reductions and tariff adjustments raising inflation concerns, a slowdown looms. We’re prioritizing high-quality fixed income to strengthen portfolios against instability, well-positioned to benefit if rates fall, given longer call dates. Recent speculation of earlier rate cuts highlights the market’s current value. Amid tariff uncertainty, we believe locking in yields now is a prudent step for clients.

Statistical Highlights

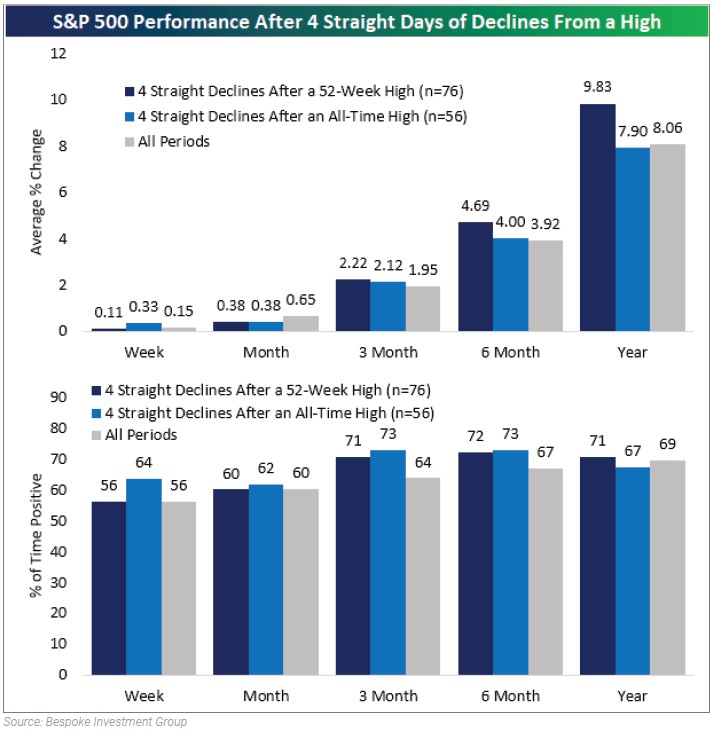

The S&P 500 hit a 52-week high on 2/19, then dropped 3% over four consecutive declines. Since 1952, such four-day slides after a peak have occurred 76 times. Uniquely, this pullback fell below the 50-day moving average (DMA), a rare event with only seven prior instances. Short-term returns post-dip exceed typical gains; six-month returns align with averages and stay positive. Yet, one-year returns show a median loss, with gains less frequent. While these reversals suggest turning points, they historically resolve upward.

Power of Planning

For investors, a financial plan is a powerful tool—preserving wealth, driving growth, and aligning resources with your ambitions. Our team shapes a bespoke strategy, tailored to your unique goals and needs, while streamlining cash flow, helping optimize taxes and manage risk. Adaptable to market shifts and life’s turns, we transform complexity into confidence.

DISCLOSURE

This material is not a recommendation as defined in Regulation Best Interest adopted by the Securities and Exchange Commission. It is provided to you after you have received Form CRS, Regulation Best Interest disclosure and other materials. This brochure is intended for informational purposes only. All information provided and opinions expressed are subject to change without notice. No part of this brochure may be reproduced in any manner without the written permission of Oppenheimer & Co. Inc. (“Oppenheimer”). Oppenheimer Asset Management Inc. and Oppenheimer Trust Company of Delaware are indirect wholly owned subsidiaries of Oppenheimer Holdings Inc., which also is the indirect parent of Oppenheimer & Co. Inc. Securities are offered through Oppenheimer. 7687504.1